文章详情

Ai全自动编写策略:SAR布林带多阶段策略(通达信&python双源码)

松鼠Quant

2025-11-05

工具推荐

『正文』

ˇ

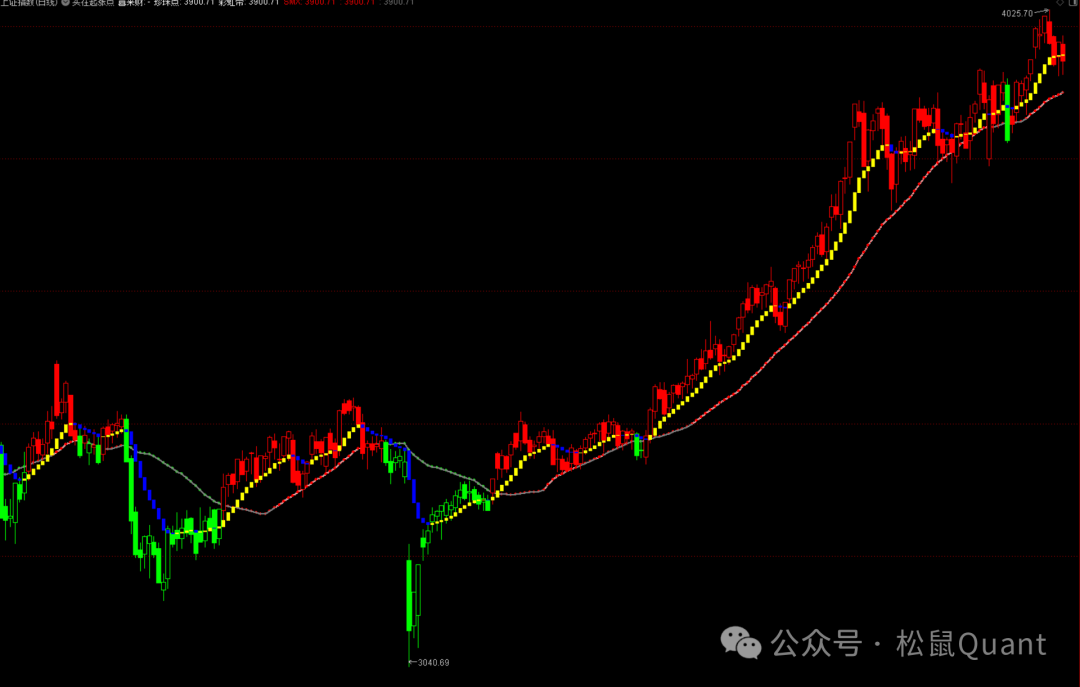

VAR1:=1090630;喜来财:DRAWNULL,NODRAW;珍珠点:IF(DATE<=VAR1,SAR(4,2,20),MA(CLOSE,30)),NODRAW,COLORWHITE;彩虹带:MA(CLOSE,30),COLORWHITE,LINETHICK2;SMX:MA(CLOSE,30),COLORRED;A:=珍珠点,NODRAW;B:=(MA(CLOSE,30)-REF(MA(CLOSE,30),1))*100/REF(MA(CLOSE,30),1);{以下是在k线图上画sar指标线}IF(CLOSE>=A,A,DRAWNULL),POINTDOT,COLORRED,LINETHICK4;IF(CLOSE<A,A,DRAWNULL),POINTDOT,COLORGREEN,LINETHICK4;IF(MA(B,3)<0.1,MA(CLOSE,30),DRAWNULL),COLORGRAY,LINETHICK2;{划彩色k线}STICKLINE(C>=A AND C>=O,C,O,2.8,1),COLORRED;STICKLINE(C>=A AND C<O,C-0.003*C,O,2.8,0),COLORRED;STICKLINE(C>=A ,H,C,0,0),COLORRED;STICKLINE(C>=A ,O,L-0.003*C,0,0),COLORRED;STICKLINE((C<A AND C>=O),C,O,2.8,1),COLORGREEN;STICKLINE((C<A AND C<O),C-0.003*C,O,2.8,0),COLORGREEN;STICKLINE(C<A ,H,C,0,0),COLORGREEN;STICKLINE(C<A ,O,L-0.003*C,0,0),COLORGREEN;JJ:=(CLOSE+HIGH+LOW)/3;A8:=EMA(JJ,10);B8:=REF(A8,1);持股区域:STICKLINE(A8>B8,A8,B8,2,0),COLORYELLOW;持币区域:STICKLINE(A8<B8,A8,B8,2,0),COLORBLUE;

github地址(国外):

https://github.com/songshuquant/ssquant-ai

gitee地址(国内):

https://gitee.com/ssquant/ssquant-ai

github地址(国外):

https://github.com/songshuquant/ssquant-ai

gitee地址(国内):

https://gitee.com/ssquant/ssquant-ai

防迷路

微 信|小松鼠-松鼠Quant

微信号|viquant01

分享